The Ecosystem's Feedback Loops

Why the Dysfunctional Equilibrium Persists

Six feedback loops

The preceding sections have described the ecosystem's characteristics, acceleration challenges, and knowledge gaps. This section asks a different question: not what the problems are, but why they are so structurally persistent. Why does an ecosystem that has been extensively diagnosed, extensively funded, and extensively programme-supported continue to produce the same dysfunctional outcomes?

The framework for analysing this kind of persistent dysfunction sits in the systems-thinking tradition. Donella Meadows' Thinking in Systems - the most accessible contemporary treatment of systems dynamics - defines a system as a set of elements interconnected in a way that produces a characteristic pattern of behaviour. The pattern is not a property of the elements; it is a property of the connections between them. When the connections are reinforcing, small initial differences amplify into stable equilibria. When the equilibrium is dysfunctional, intervening on the elements without intervening on the connections produces no durable change. Greif and Laitin's American Political Science Review paper on endogenous institutional change extends the framework: equilibria are sustained by quasi-parameters (slow-changing conditions outside the equilibrium itself) whose drift either stabilises or destabilises the configuration. The African scaling ecosystem's dysfunctional equilibrium is structurally stable because the connections between actors produce the patterns observed - and the quasi-parameters that would destabilise it have, until recently, been moving in the wrong direction.

Thomas Schelling's Micromotives and Macrobehaviour named the analytical move this section makes. Individually rational behaviour can produce collectively irrational outcomes when the actors are connected in particular ways. Each actor in the African scaling ecosystem is responding rationally to the incentives they face. The ecosystem-level outcome - programme-rich, capability-thin, structurally unable to produce scaling at the rate the diagnosis demands - is the aggregated consequence of individual rationality operating through specific feedback structures.

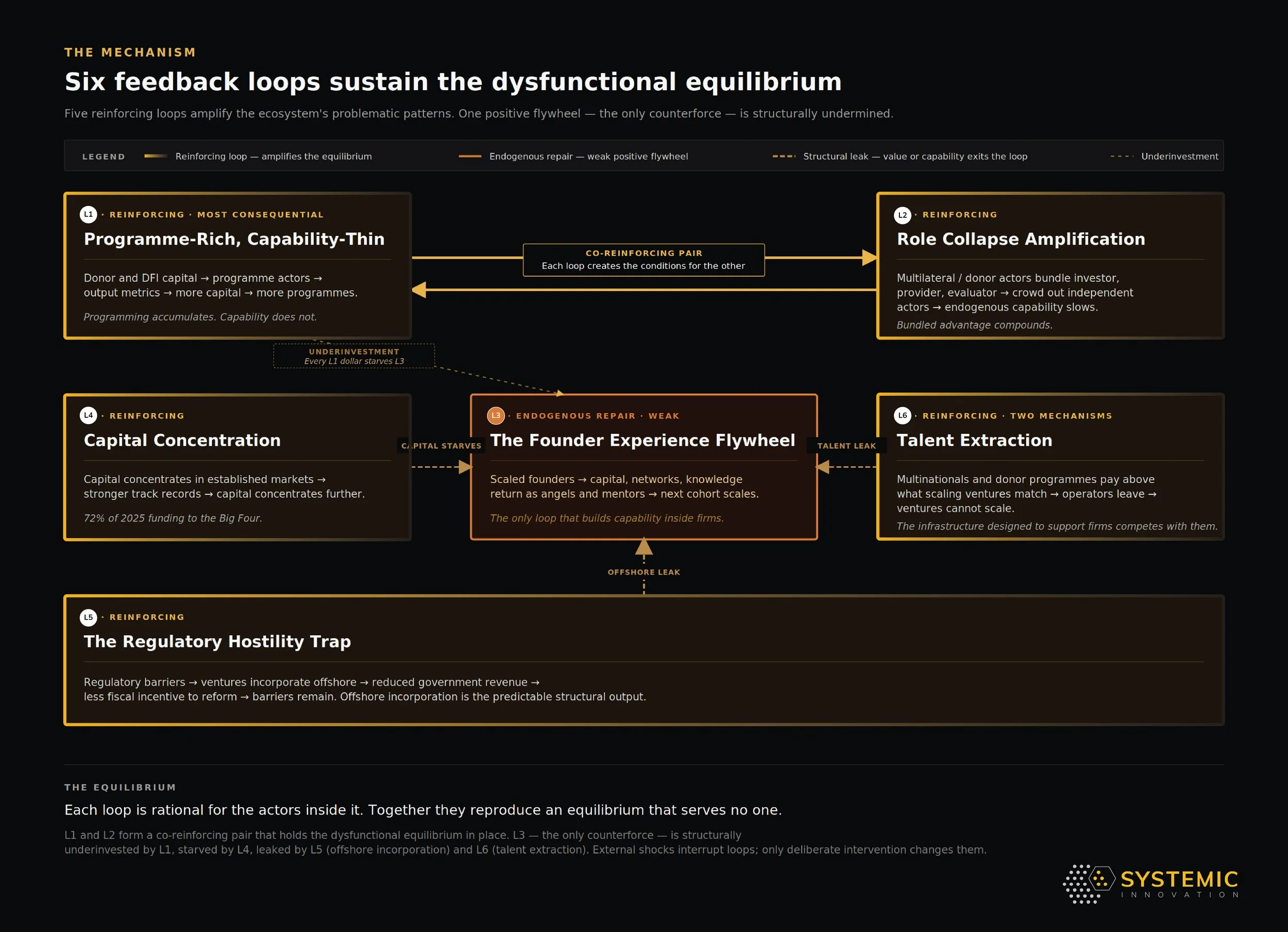

The three system structures developed earlier in this publication operate through six feedback loops. Five reinforce the equilibrium. One - the founder experience flywheel - is the only counterforce inside the system, and it is structurally undermined by the others. Each loop is rational for the actors inside it. Together they reproduce an equilibrium that serves no one. L1 and L2 form a co-reinforcing pair. L3 is starved by L1, drained by L4 and L6, and leaks through L5. External shocks - like the 2022–24 correction - can interrupt loops temporarily. Only deliberate intervention in the loop mechanisms changes them permanently.

Loop 1: The Programme-Rich, Capability-Thin Reinforcing Loop

The most consequential loop in the African scaling ecosystem runs as follows. External capital enters the ecosystem through donor and DFI programme funding. Programme actors design and deliver activities - accelerators, competitions, training, workshops. Programme outputs are measured and reported: participants trained, cohorts graduated, events held. Positive output metrics attract more external capital. More programme actors enter the ecosystem. Competition for programme mandates increases. Programme design optimises further for output legibility rather than scaling outcomes. The ecosystem accumulates more programming without accumulating more capability. Ventures scale at the same rates as before. The case for more programming appears to be confirmed by the continuing scarcity of scale-ups. External capital continues to flow into programmes.

The structural mechanic at work is a principal-agent failure. Dan Honig's Navigation by Judgment - the contemporary foundational treatment of donor-agency performance - names it precisely. When principals (donors) cannot directly observe outcomes, contracts are written on observable outputs. Agents (ESOs) optimise for what is contractually measured. The gap between observable outputs (programmes delivered) and the desired outcome (capability accumulated, ventures scaled) becomes structural rather than incidental. Honig's empirical contribution is the demonstration that this output-optimisation pattern produces worse outcomes than higher-trust contracting in environments - like ecosystem support - where the measurement-to-outcome mapping is weak. The donor architecture funding the African ecosystem is built on the assumption that tight output measurement produces accountability. Honig's evidence suggests it produces output-optimisation instead.

This loop explains why the African scaling ecosystem has become programme-rich and capability-thin despite years of intensive support. It is not a failure of intention. It is the predictable output of an incentive structure that rewards programme delivery rather than capability development, and that measures success through outputs that programmes can control rather than outcomes that only ventures can produce. The substantive design-failure treatment sits in (Stalled) Acceleration; the implication for systems analysis is that fixing programme design within the existing donor architecture cannot break this loop. The architecture itself produces the dysfunction.

TheWDI East Africa study documents this loop at the ESO level with granular precision: grant overreliance turns ESOs into implementers of donor mandates rather than strategic leaders, donor output metrics drive cohort scale over venture quality, and the resulting low-value programming produces training fatigue among entrepreneurs - who then cycle through multiple programmes without the capability development that would make them less dependent on programme support.

Loop 2: The Role Collapse Amplification Loop

The second reinforcing loop amplifies the first by crowding out the independent actors who would otherwise develop endogenous ecosystem capability. Multilateral, bilaterals, and foundations enter the ecosystem with capital, convening power, and institutional legitimacy. They accumulate bundled advantage by performing investor, programme provider, and evaluator functions simultaneously. This bundled position makes them structurally more competitive than independent ecosystem actors for talent, contracts, and influence. Independent ecosystem actors - local accelerators, research institutions, advisory firms - find themselves unable to compete on equal terms. The ecosystem's capability development function concentrates further in the hands of actors whose institutional incentives are not aligned with capability development. Endogenous capability growth slows. The case for continued multilateral and donor presence appears to be confirmed by continuing ecosystem weakness. Multilateral and donor actors maintain or expand their position.

The substantive treatment of role collapse - the structural mechanism by which a single actor performs investor, convenor, and service-provider functions that mature markets keep institutionally separate, and the resulting bundled advantage - sits in Political Economy Ecosystem. The implication for feedback-loop analysis is that role collapse is not a programme-design problem. It is a structural property of the actors involved that programme reform cannot address.

The interaction of Loops 1 and 2 is co-dependent. The programme-rich, capability-thin loop creates the ecosystem conditions in which role collapse is most likely. Role collapse amplifies the programme-rich, capability-thin dynamic by crowding out independent actors. These two loops function as a co-reinforcing pair that makes the dysfunctional equilibrium extremely stable. Interrupting either one alone will be counteracted by the other. TheDGGF systemic review corroborates this from five markets: the combination of restrictive donor funding, competitive RFP structures, and weak public-private collaboration produces exactly the fragmented, low-capability ESO landscape that Loop 1 predicts and Loop 2 perpetuates.

Loop 3: The Founder Experience Flywheel

The third loop is the ecosystem's endogenous repair mechanism - the process by which successful outcomes compound into greater future capacity. Founding teams with relevant prior experience build ventures with higher scaling probability. A higher proportion of these ventures reach scale. Scaled founders accumulate capital, networks, and operational knowledge. Some of this capital, network access, and knowledge returns to the ecosystem as angel investment, mentorship, and board-level expertise. Earlier-stage ventures accessing this resource have higher scaling probability. More ventures reach scale. The stock of experienced scaled founders in the ecosystem increases. The intensity of the positive flywheel increases.

The substantive theoretical foundation for this dynamic is treated in Defining Scale - the regional-economics literature on the Multiplier Effect (Saxenian on Silicon Valley vs Route 128, Klepper on industrial spinoff dynamics, Endeavor's empirical extension to contemporary ecosystems). The implication for feedback-loop analysis is that this is the only loop in the system that builds capability inside firms rather than in the support architecture around them.

The correction period has, paradoxically, increased the stock of experienced operators available to feed this loop - more founders have navigated the full cycle, including the difficult parts. Endeavor Insight's mapping of the Kenyan entrepreneurship network documents this compounding dynamic directly: high-growth founders connected into dense local networks drive far more job creation and follow-on investment than similarly successful but disconnected peers, and the network effects intensify as the cohort of experienced founders grows.

But Loops 1 and 2 consistently underinvest in the conditions that make Loop 3 operate effectively: they fund programmes rather than people, activities rather than institutions, and external interventions rather than internal capability. The Sustain Impact report identifies the structural consequence precisely: every dollar that flows through prescriptive programme funding is a dollar not available for the organisational development - the people, culture, governance, and systems - that makes ESOs capable of routing experienced founder knowledge back to the next generation of ventures. Every marginal dollar that flows through Loop 1 is a dollar that does not flow through Loop 3.

Loop 4: The Capital Concentration Balancing Loop

This is the ecosystem's most visible stabilising dynamic - it explains why geographic and sectoral concentration in African venture capital is so persistent despite widespread recognition of its costs. Capital concentrates in markets with established track records - Kenya, Nigeria, South Africa, Egypt. Ventures in these markets have better access to capital. They scale more successfully. They generate stronger track records. Capital concentrates further in these markets. New market entry by capital becomes less attractive relative to doubling down in established markets. Ventures in emerging markets face higher capital costs. They scale less successfully. Track records remain thin. Capital concentration continues.

The substantive theoretical foundation - Myrdal's cumulative causation and Krugman's New Economic Geography on why economic activity, once concentrated, attracts more activity through self-reinforcing dynamics - is treated in Spatial Scaling Dynamics. The implication for feedback-loop analysis is that capital concentration is not a market imperfection. It is the predicted output of standard spatial-economic theory operating through ecosystem-specific feedback structures. The Partech 2025 Africa Tech Venture Capital Report confirms the empirical pattern: despite years of calls for broader geographic distribution, the Big Four - Kenya, South Africa, Egypt, Nigeria - accounted for 72 percent of total funding (equity and debt combined) in 2025, up from 69 percent in 2024 - and 81 percent of equity funding specifically, up sharply from 67 percent in 2024. The correction period tightened rather than loosened concentration, and tightened equity concentration much more sharply than headline figures suggest. Under capital stress, risk-averse investors consolidate into familiar markets with established track records. The correction period tightened rather than loosened concentration. Under capital stress, risk-averse investors consolidate into familiar markets with established track records. The sectoral dimension operates the same way: fintech's dominance across African venture capital is not simply a reflection of investor preference. It is a product of this balancing loop. Emerging sectors face the full force of this stabilising dynamic, with unfamiliar risk profiles compounding the geographic concentration effect.

Loop 5: The Regulatory Hostility Trap

This balancing loop operates at the intersection of venture scaling and government regulatory capacity, and explains why regulatory reform is consistently promised and inconsistently delivered. Scaling ventures encounter regulatory barriers. Regulatory burden increases the cost and risk of scaling. Some ventures route around regulation through offshore incorporation - a structural response treated substantively in Political & Regulatory Barriers and Offshoring African Startups: Beyond Founder Choice. Offshore incorporation reduces the venture's tax footprint and regulatory accountability in the home jurisdiction. Government revenue from the scaling sector is less than it would be if ventures were locally incorporated. Government has less fiscal incentive and institutional knowledge to reform regulation for local ventures. The regulatory environment remains hostile. Scaling ventures encounter regulatory barriers.

Albert Hirschman's Exit, Voice and Loyalty names what is happening structurally. Faced with declining institutional quality, actors have three options: exit (leave the institution), voice (advocate for reform from within), or loyalty (accept the decline). Hirschman's central finding: when exit is available and easy, voice atrophies. Founders who incorporate offshore have exited the domestic regulatory institution. The voice that would otherwise advocate for domestic regulatory reform - the political constituency for doing the hard work of fixing the regulatory environment - is structurally weakened by the availability of the offshore exit. Each marginal exit raises the cost of the remaining voice and reduces the political pressure for institutional improvement.

This loop has a particularly important second-order effect on the founder experience flywheel. Founders who incorporate offshore become less embedded in local regulatory debates, less likely to advocate for domestic regulatory reform, and less likely to return their capital to local ventures as angel investors. The regulatory hostility trap creates a structural leak in the positive flywheel by routing successful founders toward international financial and legal infrastructure rather than local ecosystem infrastructure. Loop 5 does not just sustain itself. It actively drains Loop 3.

Loop 6: The Talent Extraction Loop

Two distinct but structurally connected mechanisms extract African technical and operational talent from the scaling venture ecosystem before the Founder Experience Flywheel has turned fast enough to replenish itself.

The first is multinational extraction. Global technology companies establish developer centres in Nairobi, Lagos, and other African primary cities, accessing high-quality technical talent at costs substantially below what equivalent capability commands in their home markets. The developer centre offers compensation, international credential recognition, and career stability that early-stage ventures cannot match. The cohort that would become second-generation African scaling operators works for international employers instead. The substantive treatment of the AI-talent layer of this dynamic sits in What AI changes about African scaling; the implication for feedback-loop analysis is that the talent extraction mechanism intensifies in AI specifically because the compensation gap between hyperscaler training centres and African ventures is widest in this segment.

The second is donor programme extraction - less visible and more structurally ironic. Bilateral programmes and multilateral agencies offer salaries, international exposure, and career credentials that scaling ventures equally cannot match - while being funded precisely to support those ventures. The person who should be the CFO of a Series A fintech becomes the programme manager of a donor-funded accelerator instead. The talent the ecosystem needs to build scaling ventures is absorbed by the infrastructure nominally designed to support them. The Misaligned Incentive Engine operates at the human capital level: the same actors whose institutional incentives reward programme delivery over scaling outcomes also outcompete scaling ventures for the operational talent that would produce those outcomes.

A further variation of this dynamic is worth naming directly: bilaterally funded programmes that actively orient African ventures toward offshore capital markets and foreign incorporation - helping founders raise in London rather than build in Nairobi - accelerate the Loop 5 dynamic while presenting themselves as ecosystem support. The orientation is not neutral. It compounds offshore dependency rather than reducing it.

The ventures most exposed are those in the scaling phase, where operational management depth is the binding constraint - the very ventures that Loop 3 depends on to generate the experienced founder cohort the next generation needs. The Founder Experience Flywheel leaks through offshore incorporation at the capital level (Loop 5) and through talent extraction at the human level (Loop 6) simultaneously. The two leaks compound. A scaled venture that incorporates offshore and loses its operational management to a donor-funded programme is structurally unable to feed the flywheel through either capital or capability transfer.

Breaking this loop requires two distinct interventions. For the multinational dimension: domestically viable equity instruments and structured alumni networks that make scaling experience compound into career value. For the donor programme dimension: conditionality requiring that programme staff are genuinely additional to - not drawn from - the pool that scaling ventures compete for.

Where are the leverage points?

Donella Meadows' twelve leverage points can be grouped, for the purposes of this analysis, into five clusters from lowest to highest leverage. This has become the reference framework for systems-change practitioners across development finance and ecosystem design. Her central insight: most interventions in complex systems are made at the lowest leverage points (changing parameters within existing structures) when the highest leverage points (changing the paradigm the system serves) would produce categorically different outcomes. Meadows wrote it as an explicit warning against the well-intentioned intervention pattern she observed in development practice: doing more of what does not work, harder, with better measurement.

Elinor Ostrom's work on polycentric governance and commons management - for which she received the 2009 Nobel Prize in Economics - adds the political-economy dimension Meadows' framework does not directly address. Ostrom's empirical finding from decades of comparative case research: collective-action problems are not solved by external regulation or by individual incentive design alone. They are solved by institutional arrangements that allow the actors closest to the problem to develop, monitor, and enforce their own rules - provided the institutional framework permits it. The implication for African scaling ecosystem design is direct: the highest-leverage intervention is not better-designed external programmes. It is institutional architecture that allows ecosystem actors to develop their own coordinating arrangements without donor architecture preempting them.

The fragmentation of African ESO systems is a paradigm-level problem: short grant cycles, intermediary competition, and funder demand for standardised metrics reinforce each other in a self-perpetuating dynamic that no amount of better-designed programming can break. The six-loop analysis suggests the following priorities.

Lowest leverage

Adding more of what the system already produces: more programmes, more accelerators, more competitions, more reports. These interventions flow with the existing loops rather than against them.

Low-medium leverage

Changing the parameters within existing structures: more capital, faster regulatory processes, better-designed programmes. These improve the performance of the existing system without changing its structure.

Medium leverage

Changing the feedback loops themselves: creating measurement systems that generate learning rather than justification; introducing independent evaluation that holds actors accountable for outcomes rather than outputs; building platforms that route experienced founder knowledge to earlier-stage ventures. The DGGF systemic review's four leverage points - financial diversification, shared data and impact measurement, human resource quality, and cross-sector stakeholder collaboration - all operate at this level.

High leverage

Changing the goals the system is organised around: shifting from programme delivery to capability development as the primary metric of ecosystem support effectiveness; shifting from startup creation to scaling outcomes as the primary measure of ecosystem health.

Highest leverage

Changing the paradigm that underlies the system: shifting from a development assistance paradigm - in which the ecosystem's problems are addressed by external actors providing external solutions - to a stewardship paradigm in which institutional actors are accountable for the long-term health of the system, not for the delivery of their own programmes. This is the deepest and most powerful intervention available. It is also the most difficult, because it requires the dominant actors in the system to voluntarily reduce their own power and presence in favour of a system that is less dependent on them. The first step is to admit how the actors who fund, deliver, and evaluate ecosystem support may be contributing to the dysfunction - asking how their incentives, reporting requirements, and data demands may be reinforcing the fragmentation they nominally seek to resolve.

The ecosystem will not change at the lowest leverage levels. The twenty recommendations of the 2022 publication operated primarily at the low-medium leverage level - they proposed better-designed versions of existing interventions. The analysis here suggests the ecosystem requires intervention at the medium-to-high leverage levels at minimum, and at the highest leverage level if the goal is genuine structural transformation.

The correction period as a natural experiment

The 2022–25 funding contraction provided an unplanned experiment in what happens when Loop 1 is interrupted by external force - but it was not one shock. It was two, operating on different timescales and with different structural implications.

The first was the VC contraction of 2022–24. Programme infrastructure whose participants depended on a continuous pipeline of investable ventures found itself without the downstream demand that justified its existence. Many hubs and accelerators closed. The ecosystem was forced, temporarily, to operate more heavily on its endogenous resources.

The second was the collapse of donor funding - structurally slower-moving but more consequential for Loop 1 specifically, because donor capital is the direct fuel of the programme-rich dynamic. The substantive treatment of the ODA contraction sits in Lessons from the Correction and Capital Systems; the implication for feedback-loop analysis is that the 23.1 percent fall in ODA in 2025 - with a further 5.8 percent contraction projected in 2026 - is not a temporary cycle. It is restructuring downward.

This matters for the feedback loop analysis in two ways. First, it directly interrupts Loop 1: the programme capital that sustains the programme-rich, capability-thin dynamic is contracting at a pace and structural depth that VC recovery alone will not replace. Second, it tests whether the ESO field responds to the shock by diversifying revenue and building organisational resilience - the reform the Sustain Impact report has been calling for - or whether it simply contracts and waits for funding to return.

The Greif-Laitin framing applies here. The ODA contraction is a quasi-parameter drift - a slow-changing condition outside the equilibrium itself whose movement either stabilises or destabilises the configuration. Until 2024, the quasi-parameters of the African ecosystem support architecture (donor budget growth, ODA priorities, programme-funding norms) drifted toward stabilising the dysfunctional equilibrium. From 2025 onward, those quasi-parameters drift in the opposite direction. The equilibrium that has been stable for two decades is becoming structurally less stable, not because the actors inside it are reforming, but because the conditions that sustained it are eroding.

The results of the VC shock were instructive on ventures. Ventures that survived were disproportionately those with endogenous capability: sound unit economics, strong management teams, durable product-market fit, and operational systems that did not depend on continuous capital infusion. These are precisely the outcomes that Loop 3 - the founder experience flywheel - is designed to produce. Ventures that failed were disproportionately those whose growth had been primarily capital-funded: optimised for fundraising metrics rather than operational performance, dependent on continuous VC subsidy, expanded geographically ahead of operational readiness. These are the outputs of an ecosystem operating through Loop 1.

The resilience of local capital through the VC downturn is the most important empirical signal the correction period produced for Loop 3. African investor capacity held while international capital fled - but the domestic surge is dominated by African DFIs, corporates, and state-backed bodies rather than commercial institutional capital. The ecosystem's improved resilience to external sentiment cycles is genuine but not yet equivalent to the commercial capital independence a mature ecosystem requires.

What the correction period did not do is change the system structure. As private capital has returned - more modestly, more selectively, but returned - the same loops have resumed operation. Programme activity is rebuilding. Role collapse is resuming. Geographic concentration has increased. The donor shock, by contrast, is not a temporary interruption. The ODA contraction is structural, politically driven, and on current trajectories will persist through the decade. This creates an unusual and arguably irreversible pressure on Loop 1: the external capital that has sustained programme-rich, capability-thin dynamics for two decades is no longer reliably available.

That pressure is either an opportunity or a threat, depending on whether the ecosystem's support actors respond by building the organisational depth and revenue diversification that the Sustain Impact framework describes - or by contracting to a smaller version of the same model and waiting for funding to return. This is the most important lesson of the correction period for systems analysis: external shocks can interrupt loops temporarily but cannot change them permanently. The donor shock is more likely to force structural change than the VC cycle ever was. Whether that change runs toward capability and sustainability, or toward collapse, depends on deliberate intervention in the loop mechanisms themselves.