Who captures value and who does not

AI does not introduce new dynamics into the African scaling ecosystem. It accelerates the dynamics already present.

Where the loops are positive, AI compounds them. Where they are negative, AI deepens them. Of the six loops, AI strengthens one. The asymmetry is the central finding.

AI's diffusion through the African scaling ecosystem is not net-neutral. It is structurally weighted toward outcomes that compound the architecture's existing failures. The capability trap, the misaligned incentive engine, and the capital architecture mismatch operate independently of AI; AI deployed within those structures reproduces them in higher resolution. The same logic operates one level up. AI changes what structural interventions are practically achievable. It does not dissolve the structures themselves.

Three infrastructure logics, three lock-in profiles

The three named African infrastructure commitments are not interchangeable. Cassava Technologies' partnership with NVIDIA - up to $720 million across South Africa, Egypt, Kenya, Morocco and Nigeria, including 12,000 GPUs over three to four years - is GPU access bundled with platform dependency: African ventures that obtain compute through the partnership obtain it through NVIDIA's stack, with foundation-model architecture switching costs absorbed at venture level. IFC's $100 million debt facility to Raxio Group, one of the Corporation's largest African digital-infrastructure investments, is concessional capital tied to ESG and operational covenants - the leverage runs through governance, not hardware. Microsoft's ZAR 5.4 billion South African commitment is a talent pipeline tied to cloud-platform commitment - the practitioners trained on Azure tooling produce dependency at the human-capital layer. Three commitments, three structurally different lock-in profiles. The shape of African AI value capture in the next decade depends on which mix of these terms African ventures negotiate.

The dependency precedent is recent and concrete. Huawei and ZTE supplied between 40 and 70 percent of Africa's 4G telecommunications infrastructure, enabling rapid connectivity expansion but creating long-term dependencies in equipment, maintenance ecosystems and vendor standards that have proved difficult to unwind. That dependency was not strategic surrender. It was the cumulative effect of procurement decisions optimised for unit cost and deployment speed within individual projects, without a framework for evaluating systemic lock-in across the sector. Cloud infrastructure, foundation-model APIs, and platform-based data processing carry the analogous risk at greater strategic depth: switching costs are embedded not in hardware but in data formats, model architectures and institutional workflows. The pattern reproduces by default if procurement is conducted project-by-project at lowest qualified bid.

The bargain that has not been struck

The Africa Declaration on Artificial Intelligence, adopted in Kigali on 4 April 2025 and aligned with the AU Continental AI Strategy, proposes a $60 billion Africa AI Fund. The AU Continental AI Strategy sets out the policy architecture; the AU's May 2025 press release reaffirms the political commitment. Seemingly, no capital has been committed. No fund manager has been appointed. No anchor LPs have been publicly named. The AfDB–UNDP follow-on commitment - $10 billion mobilised through 2035 - has the same structural pattern: ambition, signal, no published disbursement logic, no concessional-share clarity, no mobilisation ratio, no disbursement-linked indicators, no accountability mechanism when targets are missed.

The reframing matters. "No capital has been committed yet" misreads the architecture. Dercon's framework is the diagnosis: capital does not form against an elite bargain that does not exist. The political bargain that would mobilise sovereign-pension allocation, DFI co-investment, and private-LP commitment into an Africa AI Fund of this magnitude has not been struck. The silence is the bargain's absence, not its delay.

The absorptive-capacity sequencing problem compounds the fund-formation gap. The five-prerequisite framing - data, computing, skills, regulation, capital - makes the programme its own prerequisite. Capital cannot be productively deployed into compute infrastructure that does not yet exist, in a regulatory environment that has not been established, by a workforce that has not been trained. Without an explicit sequencing strategy - energy before compute, connectivity before applications, human capital before enterprise support - $10 billion is not an investment programme. It is a resource-mobilisation target with a horizon and no disbursement logic. The same critique applies, in larger form, to the $60 billion Kigali commitment.

The supply-side baseline confirms the constraint. The Africa Data Centres Association's 2026 Economic Report puts active capacity at approximately 360 MW against a 1.2 GW pipeline that, set against hyperscale expansion elsewhere, will leave Africa's share of global capacity broadly unchanged. WEF's Investing in Green Compute in Africa records 7 million GPU hours of unmet demand against 0.6 percent of global data-centre capacity for 18 percent of the world's population. The binding constraint underneath each of these numbers is power. Without it, no compute deployment is operable.

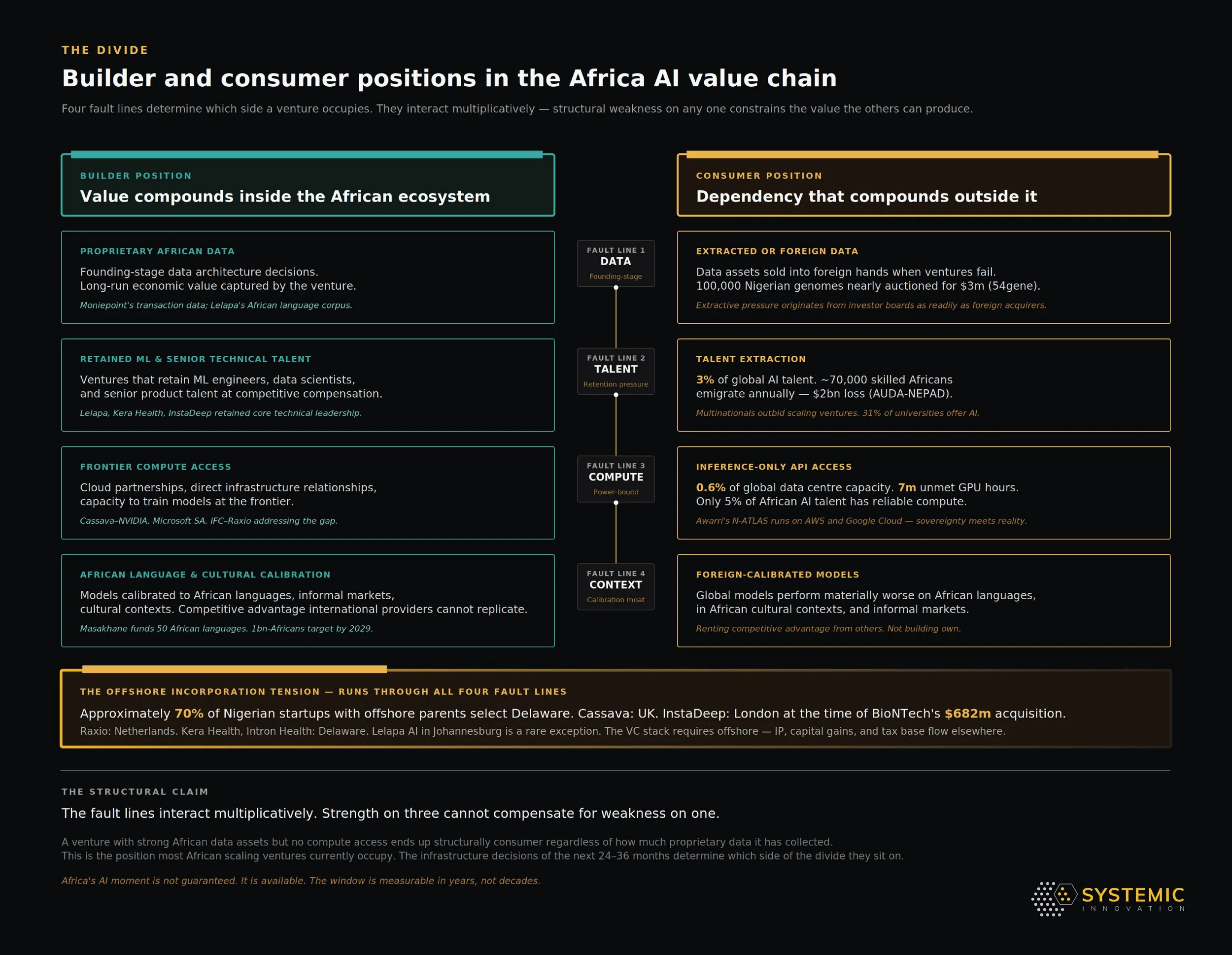

Four fault lines, four different binding constraints

The fault lines interact, as the figure shows. The binding constraint, however, differs by venture type. Lelapa AI's binding constraint is compute: the locally-incorporated commercial position is what makes the African-language work analytically distinctive, and what structurally limits frontier-scale training. InstaDeep's binding constraint, in retrospect, was data sovereignty: when the BioNTech acquisition closed at $682 million, the ongoing IP, the tax base, and the secondary data-product accumulation moved offshore with the corporate domicile. Cassava's binding constraint is infrastructure capital: the GPU deployment requires the kind of capital-stack architecture the African private-capital market does not yet form for AI-specific infrastructure. Awarri's binding constraint is sovereignty colliding with reality: the N-ATLAS Nigerian government model runs on AWS and Google Cloud because Nigeria does not yet have data centres capable of training it. Same fault lines, four different binding constraints, four different value-capture trajectories.

Value capture runs in three layers

The geography of value capture is the visible layer. It is also the shallowest. Value capture in AI runs in three layers, and the offshore-incorporation banner the figure carries is only the first.

The first layer is exit value: where the proceeds of an acquisition land. Offshore incorporation moves this layer outside African jurisdictions by default. The structural treatment is in Offshoring African Startups; the AI-specific instances are the highest-stakes case of the broader pattern.

M-KOPA illustrates the second layer: African operational data can compound inside the venture over time, even where the corporate financing or holding structure is more complex. The point is not simply where the company is domiciled, but where the data asset, underwriting logic and product-learning loop accumulate.

The third layer is the accumulation curve: the structural rate at which an African moat compounds against the rate at which non-African moats compound. A locally-incorporated venture with strong African data but no compute access does not compound at the rate of a frontier-trained competitor. The third layer is the most consequential and the least visible. The geography of value capture matters; the architecture of value capture matters more.

Stop announcing, start designing

The decisions being made now - about data architecture, compute access agreements, AI governance frameworks, and the procurement terms under which African ventures access foundation models - will shape Africa's AI value-capture trajectory for a generation. The structural question is not whether Africa will participate in the global AI economy. The continent already does, at the labour-arbitrage layer. The question is whether participation accumulates back into African ventures, African data sovereignty, and African capability - or compounds offshore as it has done in every prior infrastructure cycle. Three operational provisions would change the procurement architecture: mandatory interoperability standards for publicly financed compute, data-localisation conditions for programme-funded training pipelines, portfolio-level dependency assessments conducted across the initiative rather than within individual projects. Without them, $10 billion and $60 billion are press conferences with horizons attached.

The window is measurable in years. The cost of coordination failure is not recoverable through subsequent effort.