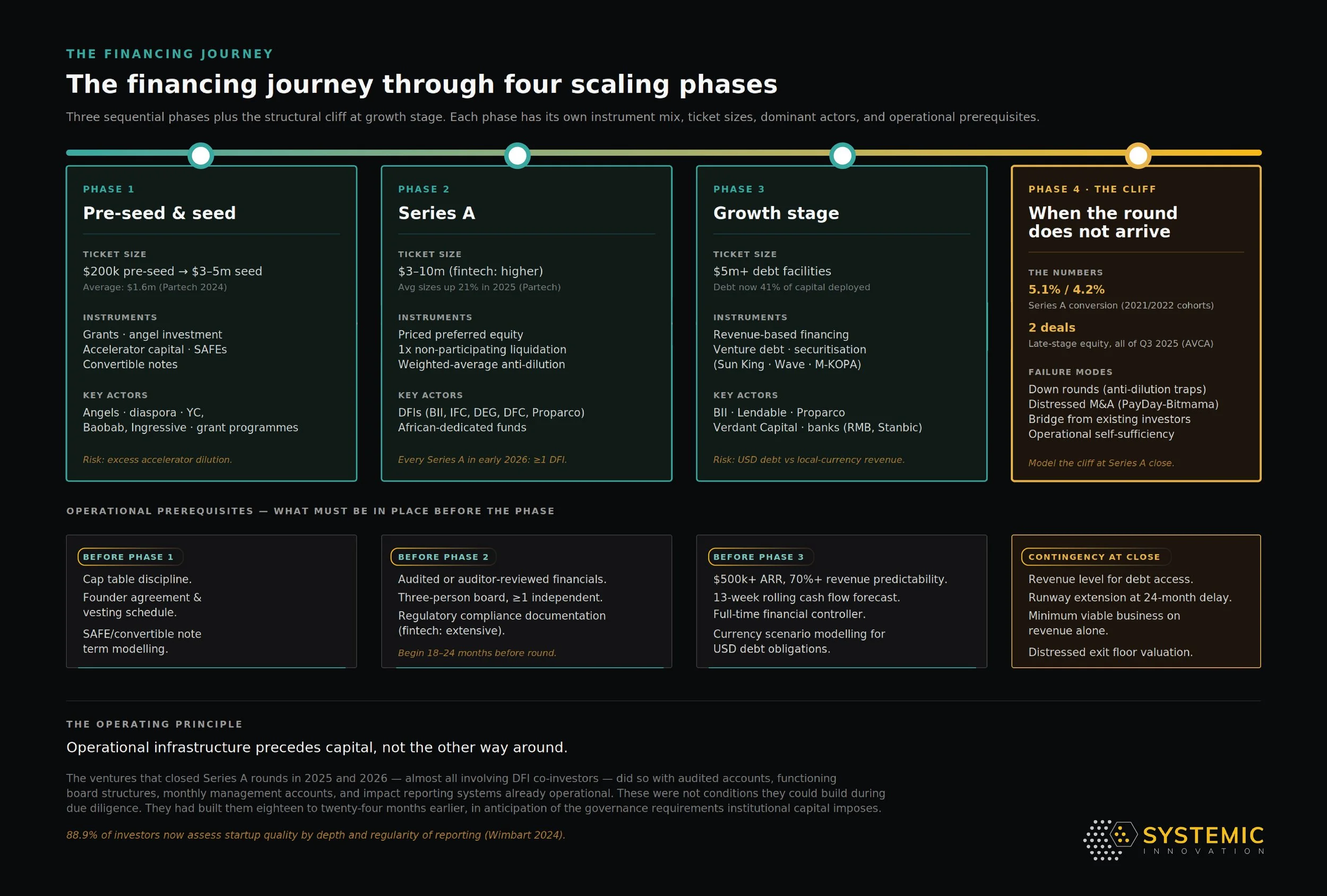

The Financing Journey Through the Scaling Phases

This section is written for founders navigating the financing journey in practice. It assumes familiarity with basic financial instruments and is more technical in register than the surrounding sections - intentionally so, because the decisions it addresses carry direct commercial consequences if made without this level of specificity.

Most treatment of African tech financing focuses on aggregate capital flows - how much was raised, by which sectors, in which markets. What it rarely addresses is the financing journey as a founder actually experiences it: what instruments are available at each phase, what each costs in dilution and governance terms, how African terms differ from global benchmarks, and what to do when the expected round does not arrive. This section addresses that gap, drawing on Partech Africa's annual reports as the primary quantitative source, and on primary research with founders, investors, and advisors across the ecosystem.

The visual architecture below establishes what each phase typically looks like. What follows is the operational depth that founder decisions actually require - phase by phase, with the African-specific departures from global VC norms made explicit.

Phase 1: Pre-seed and seed - grants, angels, and the convertible note

The pre-seed and seed phase in African markets involves a wider instrument mix than equivalent stages in the US or Europe. The institutional seed fund market is thinner, the grant and competition ecosystem more active, and the angel investing base more heterogeneous. A typical East African venture at this stage has raised some combination of: grant funding from innovation competitions, development-funded challenge programmes, or government schemes under Startup Acts now operational in eight African countries; angel investment from local high-net-worth individuals or diaspora investors; accelerator capital from programmes such as Y Combinator, the Baobab Network, or Ingressive Capital; and convertible instruments bridging toward a priced round.

The Partech 2024 Africa Tech VC Report documents average seed ticket sizes of $1.6 million - up 26 percent from the prior year, as investors consolidated into fewer but larger seed bets following the correction period. That average masks a wide range: under $200,000 at pre-seed to $3–5 million for competitive fintech or climate tech rounds. The broader global benchmark - founders at seed stage typically giving up 15–20 percent equity for standard deals, or 10–15 percent for competitive deals with strong traction per Rebel Fund's 2025 dilution analysis - applies directionally in African markets but with a documented distortion that founders entering the ecosystem for the first time rarely encounter in pre-reading.

African accelerators and early-stage investors have historically taken equity positions that are outsized relative to the capital and support provided. Y Combinator - the most internationally respected benchmark - takes 7 percent for $500,000 (a post-money SAFE structure comprising $125,000 for 7% plus a $375,000 MFN note). African accelerator programmes have ranged from 7 to 15 percent for cheques of $50,000 to $150,000, with venture-builder models such as Antler taking 10 percent for $100,000. A founder who accepts three such investments before a priced round may enter their first institutional round having already given up 35 to 45 percent of the company - before a single institutional investor has participated. That level of dilution at seed stage constrains the entire financing trajectory, because institutional Series A investors typically require 15 to 25 percent ownership, and a founder entering that negotiation with 55 percent remaining faces a structurally difficult cap table before any conversation about management team equity or ESOP. The correction period's funding contraction has begun to discipline this dynamic, but it has not eliminated it.

Most African institutional seed rounds now use SAFEs or convertible notes rather than priced equity rounds. The practical implication is that dilution is deferred to the next priced round but compressed into it.

Phase 2: Series A - the institutional anchor and what it requires

The Series A is the first round at which most African ventures encounter institutional venture capital with structured governance requirements. In the African context, this round typically ranges from $3 to $10 million for most sectors, with fintech raising somewhat more. The Partech 2024 report shows Series A average ticket sizes declining 18 percent in 2024 - a year in which the correction period's full force was felt at the institutional level. The 2025 Partech report shows meaningful recovery: Series A average round sizes up 21 percent year-on-year, with investor participation at Series A up 7 percent. The recovery in pricing has not been accompanied by a relaxation of governance requirements - if anything those have tightened, reflecting what DFIs have learned from the correction period's failure cohort.

The investor composition at Series A has structurally shifted. Reviewing the most active Series A investors across the Partech 2024 report - BII, DEG, DFC, IFC, Proparco, and AAIC are the six most active investors in African tech debt per Partech 2024, while the most active equity investors at venture stage are a different set led by Acumen, AfricInvest, Norrsken22, Partech Africa, Ventures Platform, and Visa. Launch Base Africa's 2026 analysis of early-year deal activity confirms the structural picture: every Series A recorded in the first two months of 2026 involved at least one DFI or state-backed investor. Commercial venture funds from North America and Europe - which led Series A rounds in 2020 and 2021 - have largely retreated, leaving a market dominated by African-dedicated funds and DFI co-investors. Understanding what DFIs require is therefore not a supplementary consideration for Series A preparation. It is the central preparation task.

The structural finance literature has named what DFI dominance does to the contractual architecture of Series A rounds. Kaplan and Strömberg's Review of Economic Studies paper on financial contracting between entrepreneurs and venture capitalists - the foundational empirical study of VC contract design - established the standardised architecture that has organised global venture finance since: preferred equity with liquidation preferences (typically 1x non-participating), anti-dilution protection (typically broad-based weighted-average), pro-rata rights for lead investors, vesting schedules, board representation tied to ownership thresholds, and protective provisions over a defined list of corporate actions. The contractual architecture is now sufficiently standardised globally that founders can read a YC standard term sheet and recognise its structural elements in any institutional Series A round in any market.

Lerner and Schoar's Quarterly Journal of Economics paper on VC contractual practices in international markets extends the analysis specifically to cross-border and emerging-market contexts. Their central empirical finding: VC contracts in jurisdictions with weaker contract enforcement and shallower capital markets routinely depart from the global standard architecture in ways calibrated to the institutional environment. The departures are not pathologies. They are the architectural response to the operating environment - different governance instruments, different control rights, different intermediary structures than the pure-commercial Silicon Valley template.

The African Series A configuration is exactly this kind of calibrated departure. The standard contractual architecture is followed - 1x non-participating liquidation preference, weighted-average anti-dilution, pro-rata rights for leads. The material African-specific departure is the DFI observer seat. When BII, IFC, Proparco, or DEG participate as cornerstone investors - which, as documented above, is now structurally common - they carry disclosure obligations that constrain board meeting content. These observers have reporting requirements to their own institutions that commercial investors do not have, and discussions touching on competitive intelligence, government relationships, or commercially sensitive matters may be treated differently in a DFI-observed boardroom than in a purely commercial one. Founders who have not read term sheets before receiving one should read the YC standard Series A term sheet as a comparative baseline before entering negotiations.

Three operational requirements at Series A are materially more demanding than Silicon Valley benchmarks would suggest, and founders who encounter them at term sheet stage rather than in advance lose time and sometimes lose investors entirely.

Board formalisation: most institutional African investors at Series A now expect a minimum of three board members, at least one genuinely independent, with agreed information rights and protective provisions - typically as a condition of closing, not a post-close recommendation. The substantive treatment of board governance restructure as a scaling-decision inflection point - anchored in Hermalin and Weisbach on boards as endogenous institutions, the King IV Code, and the Financial Reporting Council of Nigeria's Corporate Governance Code2018 - sits in The Scaling Decision Log Decision 3.

Financial reporting: investors expect audited or auditor-reviewed financials. Many African ventures do not have these at the point of approaching Series A. Preparing audited accounts takes three to six months from a standing start. Beginning this process after a term sheet is signed is too late. A venture that has modelled a twelve-month fundraise timeline and not started its audit process in month one has underestimated the timeline.

Regulatory compliance documentation: for fintech in particular, the compliance documentation requirements imposed by Series A investors are substantially more extensive than the venture's prior interactions with regulators have required. The IFC's Corporate Governance Toolkit for SMEs identifies poor record-keeping, tax non-compliance, and unclear shareholder arrangements as the top deterrents for global VC and DFI investors.

A founder who managed seed dilution well - two rounds of institutional seed at 15 percent total dilution, plus a modest ESOP pool - and who raises Series A at 20 percent dilution should own approximately 55 to 60 percent of the company post-Series A. A founder who accepted early accelerator equity carelessly may own 35 to 40 percent by the same point. The difference is not cosmetic: it determines whether there is enough remaining equity to incentivise the management team at Series B, whether a DFI investor can find an acceptable entry point, and whether an exit generates meaningful founder returns.

Phase 3: Growth stage - the structural shift to debt

The most significant change in African tech financing since the 2022 publication is the emergence of debt as a mainstream growth-stage instrument. The Partech 2025 report documents $1.64 billion in debt financing deployed across 107 transactions in 2025 - 41 percent of all capital deployed in African tech, up from 17 percent in 2019. Partech describes this as a structural shift, not a cyclical response: debt has entered a new phase of scale and normalisation in African tech. The trajectory is unambiguous: $350 million across 27 deals in 2019; $1.55 billion across 71 deals in 2022; $1.64 billion across 107 deals in 2025.

The instruments available at growth stage fall into three categories with different prerequisites, risk profiles, and appropriate use cases.

Revenue-based financing - capital repaid as a percentage of monthly revenue - suits ventures with predictable recurring revenue and variable cost structures, avoids dilution and security requirements, but constrains effective growth if repayment percentages are high relative to margins. The Global Innovation Fund's February 2026 analysis identifies a structural gap in the sub-$5 million range - the ticket size most useful to high-growth startups for working capital and steady expansion - which larger debt providers do not efficiently serve.

Venture debt - term loans from specialist lenders including BII, Lendable, Proparco, and Verdant Capital - typically accompanies or follows equity rounds and requires security over assets or receivables.

Securitisation - packaging recurring receivables into asset-backed instruments - has been pioneered by fintech and cleantech ventures. Sun King's 156 million securitisation in July 2025, converting PAYGO solar loan receivables into investable assets, is the most recent and largest example, building on Sun King's own 2023 $130 million Citi-arranged transaction - the first bank-led Kenyan-Shilling securitisation in Sub-Saharan Africa outside South Africa. M-KOPA's parallel use of receivables-based finance has taken the form of a $200M+ sustainability-linked syndicated debt facility (Standard Bank-led, May 2023) rather than a true securitisation. The substantive treatment of the PAYGO model as a market-creation architecture sits in Growth and Management Strategies; the implication for growth-stage finance is that the securitisation route is available only to ventures whose underlying business has produced sufficient receivables to be commercially packageable - a structural prerequisite that operational maturity, not capital availability, determines. Wave's EUR 117 million (approximately $137 million) debt facility - led by Rand Merchant Bank with BII, Finnfund, and Norfund participating - illustrates the strategic logic: Wave, serving over 20 million monthly active users across eight markets in West and Central Africa, chose debt because it was the appropriate instrument for a venture with steady, demonstrable mobile money revenues - non-dilutive, available at scale, and aligned to its cash flow profile. The prerequisite for accessing such a facility is precisely what the correction period selected for: operational maturity, governance readiness, revenue visibility, and the audit trail that institutional lenders require.

The biggest hidden risk in growth-stage debt is currency. Many African ventures borrow in dollars but earn in local currency. When the local currency falls, repayments become much more expensive even if the business is performing well. This is the practical meaning of “original sin”: firms in emerging markets are often pushed into foreign-currency borrowing because local-currency finance is too shallow, expensive, or unavailable. Partech’s 2024 Africa tech report states the problem clearly: most available debt remains USD-denominated and costly, while most ventures earn locally. During the correction period, this mismatch became severe: the Nigerian naira lost more than half its buying power between January 2023 and January 2024, while the Kenyan shilling lost 22 percent. The better model is local-currency debt for local-currency revenues. Sun King’s $80 million naira-denominated facility, structured by IFC and Stanbic IBTC, shows what this looks like. But it remains the exception. Founders taking growth debt need to model currency scenarios explicitly; the most dangerous risk may not appear in the headline interest rate.

Phase 4: The Series B cliff - when the expected round does not arrive

The Series B cliff was the most acute structural failure in the African financing landscape during the correction period. The Partech 2024 report documents the worst of it: Series B total funding fell 36 percent to $413 million; deal counts declined 14 percent; and average ticket sizes fell 27 percent. The Partech 2025 data shows meaningful recovery - Series B average round sizes up 12 percent, investor participation at Series B up 29 percent - but the structural constraint has not resolved. AVCA's full-year 2025 Venture Capital Activity in Africa report, released in February 2026, makes the structural picture starker still: of the 35 African startups that raised Series B funding between 2023 and 2024, none had progressed to Series C by the end of 2025; late-stage equity activity fell to its lowest level since 2020, with the median late-stage deal size dropping from $100 million in 2024 to $55 million in 2025. The number of investors willing and able to lead a $15–30 million Series B in African markets - with appropriate sector expertise, risk appetite, and the ability to deploy at this scale into frontier markets - is small. When those investors pass, or when a venture's metrics do not meet the threshold for growth-stage equity, the range of options is narrower than founders typically plan for.

The outcomes documented across the correction period are instructive. Down rounds - raising at a lower valuation than Series A - are legally possible but activate anti-dilution provisions that further dilute founders, signal distress to future investors, and structurally disadvantage the founder's position in subsequent governance negotiations. The Kaplan-Strömberg contractual architecture introduced earlier names what is happening structurally at this moment: the anti-dilution protection that the Series A investors required as standard contractual protection is now operating against the founder, and the protective provisions that Series A investors hold over corporate actions structurally narrow the founder's negotiating space at exactly the moment they most need flexibility.

Distressed acquisitions, in which a larger platform acquires the team and technology rather than the business as a going concern, have been a common outcome - TechCabal Insights documents over 50 M&A transactions in 2025, many driven by necessity rather than strategic value creation. The PayDay-Bitmama transaction - in which a $3 million seed-backed venture was acquired for approximately $1 million in equity after governance and operational failures - illustrates what distressed M&A means for founders who have given up equity carelessly in earlier rounds: the remaining value is thin before it is divided.

Bridge financing from existing investors can extend runway if they have both capital and conviction; TLcom Capital's stated investment philosophy - that durable African venture capital requires investors prepared to deploy through cycles, not only in bull markets - points to a gap that the correction period made visible: African-dedicated investors with the balance sheet and appetite to bridge between rounds remain scarce.

Operational readiness as a financing prerequisite

The operational implication is direct: model the Series B explicitly not arriving on schedule. That means knowing, at the point of closing the Series A, what revenue level is required to access growth-stage debt; how long Series A capital extends runway if Series B is 24 months late; what the minimum viable business looks like operating on revenues rather than investor capital; and what distressed exit options exist and at what valuation floor. The LumiBrief analysis on venture debt prerequisites suggests a practical threshold: ventures should not consider debt instruments below $500,000 ARR with at least 70 percent revenue predictability - a benchmark that reflects the minimum scale needed to service debt payments while maintaining operational flexibility in African markets where revenue volatility is structurally higher than in developed ones. The ventures that navigated the correction period made these calculations in advance. The evidence from the correction period's failure cohort - as documented by Launch Base Africa, Afridigest, and Disrupt Africa - is that the ones that failed had not.

The financing journey described in this section is inseparable from the operational infrastructure that makes it navigable. The ventures that closed Series A rounds in 2025 and 2026 - almost all involving DFI co-investors as documented above - did so with audited accounts, functioning board structures, monthly management accounts, and impact reporting systems already operational. These were not conditions they could build during due diligence. They were conditions they had built eighteen to twenty-four months earlier, in anticipation of the governance requirements that institutional capital imposes.

The practical thresholds are consistent across markets. Fractional CFO engagement should begin at $1–3 million ARR - three to six months before any significant fundraising process, not at its start. A full-time financial controller owning the monthly close is the Series A milestone; a full-time CFO is the growth-stage prerequisite. The 13-week rolling cash flow forecast - the gold standard for short-term liquidity management - should be running weekly before any investor conversation about debt facilities begins. Wimbart's 2024 survey found that 88.9 percent of investors say reporting quality significantly shapes their impression of a startup's leadership and management - sustainability metrics have become the leading investor priority at 29.4 percent, ahead of financial reporting at 22.2 percent (with operational and future KPIs each at 16.7 percent. A venture that cannot produce this reporting reliably is not investor-ready, regardless of its revenue metrics.

The organisational management infrastructure - OKR systems, management cadences, board pack discipline - follows the same logic. Andy Grove's High Output Management remains the most operationally grounded foundation for building these systems; the OKR framework as Grove introduced it at Intel used binary grading, and the 60–70 percent key-result completion norm - popularised by John Doerr's Measure What Matters and codified in Google's re:Work guidance - is a calibration that most African scale-up founders encounter backwards.. The operational specification that translates these thresholds into the specific reporting structures, management cadences, and financial systems appropriate for East African scaling ventures at each stage is developed in the EADC practitioner resources. What the analytical framework establishes is the sequence: operational infrastructure precedes capital, not the other way around. The ventures that are operationally ready when capital becomes available are the ones that close the round. The ventures that begin building operational infrastructure when capital arrives are the ones that lose it during due diligence.