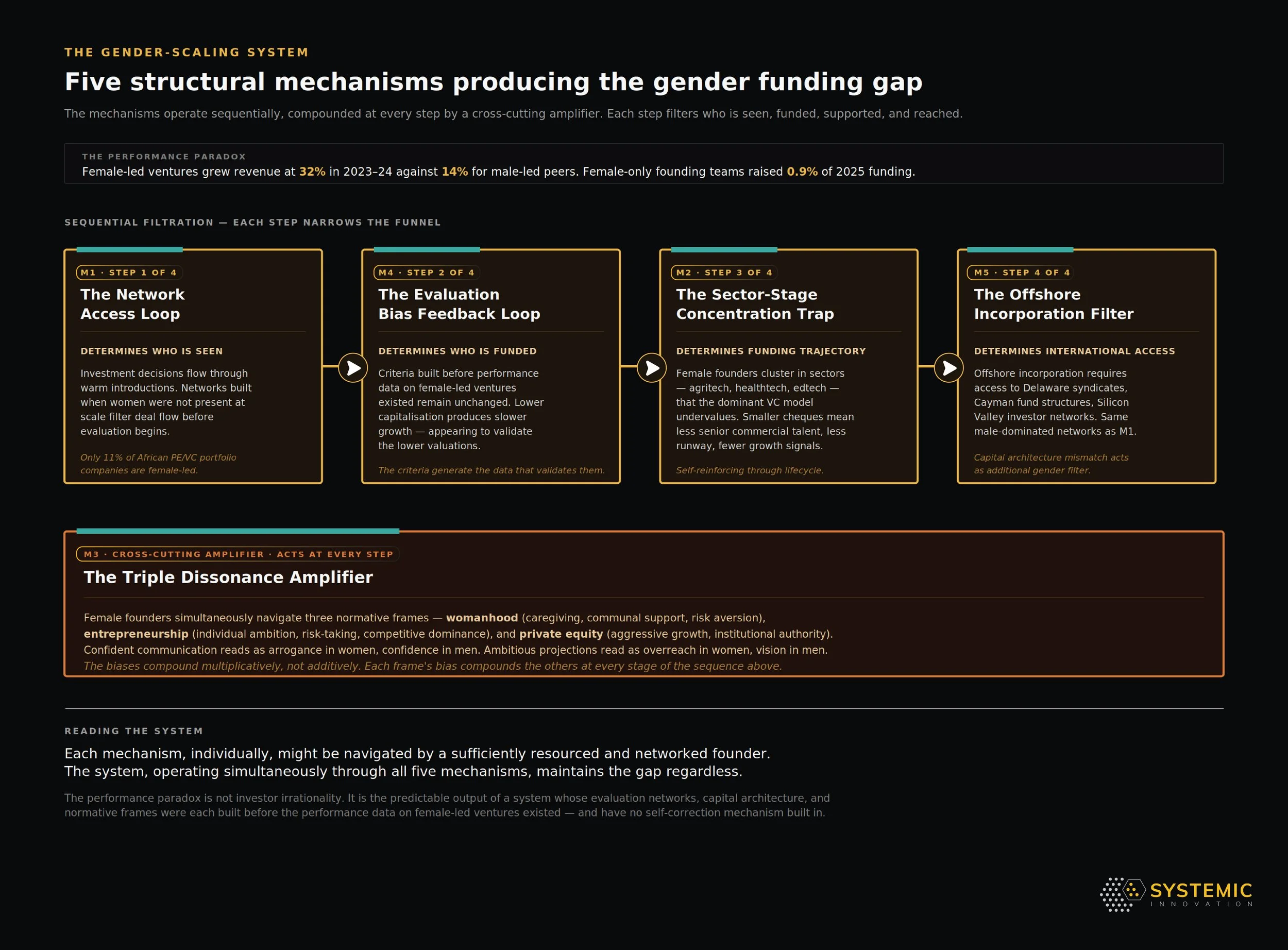

Gender-Scaling System

Why a systems account is necessary

The gender funding gap in African tech has been documented, decried, and the subject of dedicated initiatives for more than a decade. Female founders raise a small fraction of what male founders raise. The gap remains severe and, on some measures, has worsened. And the response - more gender-lens funds, more female founder accelerators, more diversity pledges - has not reversed the trend.

This is the signature of a structural problem. When a well-documented inequality persists and worsens despite sustained attention and dedicated resources, the explanation is not inadequate awareness or insufficient good intention. It is that the interventions being applied are operating at the symptom level rather than at the structural level. The substantive treatment of the gender-and-finance research foundation - drawing on Brush et al's foundational empirical work establishing that the gender funding gap is structural rather than performance-driven - sits in Founders and Leadership Teams. The implication for African-specific analysis is that the gender funding gap is not a problem of visibility or pipeline. It is a problem of system architecture.

The performance paradox makes the structural character of the problem visible. According to Africa: The Big Deal, female CEOs raised just $48 million in African startup funding in 2024 — more than four times less than in 2023, and one of the lowest levels since tracking began - against nearly $2.2 billion raised by male peers. The AVCA Gender Diversity in African Private Capital report documents that female-led portfolio companies grew revenue by 32 percent in 2023–24, against 14 percent for male-led peers; female-founded companies delivered 50 percent revenue growth over the same period. Yet women remain sharply underrepresented in portfolio leadership: only 5 percent of portfolio companies are female-founded and 11 percent are led by a female CEO.

The performance data and the allocation data point in irreconcilably opposite directions. This paradox is not explicable by individual investor irrationality or cultural bias alone. It is explicable by the system structure within which individual investment decisions are made. That structure is shown below: five mutually reinforcing mechanisms that together produce the outcome.

The five gender mechanisms

The five mechanisms are not parallel - they are sequential and interacting. The performance paradox is not investor irrationality. It is the predictable output of a system whose evaluation networks, capital architecture, and normative frames were each built before the performance data on female-led ventures existed, and have no self-correction mechanism built in.

Mechanism 1: The network access loop.

Investment decisions in venture capital are disproportionately made through warm introductions - referrals from existing portfolio founders, co-investors, and trusted advisors. This is rational from a due diligence perspective: warm introductions provide pre-screened signal about founder quality that reduces the information cost of evaluation.

Warm introduction networks are not gender-neutral. The substantive treatment of network architecture as the structural mechanism by which advantage compounds - anchored in Granovetter's "Strength of Weak Ties" and Burt on structural holes - sits in What Working Support Infrastructure Looks Like. The implication for gender analysis is direct. Networks built through professional relationships that have historically excluded women remain structurally biased toward male-founded ventures, regardless of any individual GP's commitment to gender-neutral evaluation. The AVCA Gender Diversity in African Private Capital report found that only 11 percent of portfolio companies are female-CEO-led and 5 percent are female-founded - a representation gap that compounds at every stage of the deal-flow pipeline. AVCA's separate cut on deal flow shows women-only founding teams received just 7 percent of venture capital deal volume and 2 percent of total deal value between 2020 and the first half of 2025. With most decision-makers being male, and with decision-making disproportionately occurring through same-gender social networks, the pipeline of investment opportunities that reaches a given GP is structurally biased toward male-founded ventures.

This mechanism operates regardless of explicit gender bias. A GP who is genuinely committed to gender-neutral investment can still receive deal flow that is overwhelmingly male-founded, because their network - built through the same social dynamics that have historically excluded women - systematically filters the opportunities they see. The gender gap in who is seen is prior to and independent of the gender gap in who is funded.

The network access loop reinforces itself: male-founded ventures that receive investment become the anchor portfolio companies from which subsequent warm introductions flow. The World Bank Africa Gender Innovation Lab's recent research on women-owned firms in Sub-Saharan Africa documents this pattern empirically across multiple African markets: women entrepreneurs report systematically smaller and more gender-segregated professional networks than male peers with comparable education and experience, with the network gap concentrating exactly at the senior-investor / decision-maker layer where capital allocation occurs. Without deliberate structural intervention at the network-building stage - not the funding stage - this loop will maintain the gap regardless of commitment to gender-neutral evaluation criteria.

Mechanism 2: The sector-stage concentration trap.

Female founders are disproportionately concentrated in sectors - agritech, healthtech, edtech - that receive smaller investment amounts than fintech and SaaS, and at earlier stages that attract smaller cheques than growth-stage rounds. The Partech 2025 report documents that agritech is among the few sectors approaching gender parity in equity deals, with female-founded startups accounting for 39 percent of agritech equity deals and 58 percent of agritech funding. This is the exception that illustrates the rule: female founders disproportionately build in sectors that are underweighted in the overall VC allocation.

The substantive treatment of why VC investment models systematically undervalue institutional-voids-filling sectors - anchored in Khanna-Palepu's institutional voids framework and Christensen's Prosperity Paradox on market-creating innovation - sits in Growth and Management Strategies. The implication for gender-scaling analysis is structural: the sectors in which female founders are most represented are those where the commercial opportunity is most closely tied to underserved populations. Female founders building from lived experience of gender-specific healthcare challenges, smallholder agricultural constraints, or educational access gaps are building genuine commercial opportunities - but in markets that the dominant VC model, oriented toward rapid growth in large addressable markets, systematically undervalues.

The Africa Gender Innovation Lab's empirical research across multiple African markets confirms the pattern: women-owned firms operate disproportionately in sectors with high social value and lower per-firm capital requirements, and the dominant VC investment thesis treats these characteristics as deficiencies rather than features of a different commercial logic. The EADC research programme found consistent evidence of this pattern across Kenya, Ethiopia, and Rwanda: female-founded ventures were disproportionately concentrated in sectors with strong social impact but smaller perceived total addressable markets - not because female founders lack commercial ambition but because their market knowledge is concentrated in markets that VC investment models have not yet learned to evaluate.

The sector-stage trap is self-reinforcing: because female founders raise smaller amounts at earlier stages, they have less capital to hire senior commercial talent, less runway to achieve the revenue milestones that would justify larger rounds, and less operational development to demonstrate the scaling trajectory that growth investors require.

Mechanism 3: The triple dissonance amplifier.

Female founders in African markets simultaneously navigate three normative frames: the normative frame of womanhood, which in most African cultural contexts emphasises caregiving, communal support, and risk aversion; the normative frame of entrepreneurship, which celebrates individual ambition, risk-taking, and competitive dominance; and the normative frame of private equity, which valorises aggressive growth and institutional authority.

Female founders are evaluated against the entrepreneurship frame by investors using criteria built on male entrepreneurial archetypes. Contemporary scholarship on gender bias in venture-capital evaluation - including Kanze, Huang, Conley and Higgins' field-experimental work on the prevention-versus-promotion asymmetry in investor questioning, and Onoshakpor, Cunningham and Gammie's qualitative comparative work on Nigerian women entrepreneurs and access to finance - documents the pattern empirically: confident communication is evaluated as arrogance in women but confidence in men; ambitious projections are evaluated as overreach in women but vision in men; market-creation strategies grounded in lived community experience are evaluated as social-impact rather than commercial bets. Each frame's evaluation operates on different criteria; female founders are simultaneously held to multiple and conflicting standards.

The triple dissonance is not simply additive - it is multiplicative. Each frame's bias compounds the others. This mechanism explains why dedicated gender-lens funds have not solved the problem. They address one dimension - providing a space in which female founders are not evaluated through the male entrepreneurship archetype. But they do not address the network access loop, and they do not address the sector-stage trap. Gender-lens funds that invest in female founders in health and education sectors at pre-seed are not providing the growth-stage capital that would enable those founders to demonstrate scaling trajectories.

Mechanism 4: The evaluation bias feedback loop.

Investment evaluation criteria are not gender-neutral, and the criteria themselves generate a feedback loop that compounds the disadvantage. The feedback loop operates because the criteria generate the data that validates them. If female founders consistently receive smaller investments, their ventures grow more slowly and produce smaller exits - not because female founders run worse businesses, but because undercapitalised businesses grow more slowly. These outcomes then appear to validate the lower valuations and smaller investment amounts that generated them.

The substantive treatment of how dysfunctional equilibria sustain themselves through self-reinforcing dynamics - anchored in Greif and Laitin on endogenous institutional change - sits in Feedback Loops. The implication for the gender-scaling system is that the evaluation-bias feedback loop is structurally identical to the broader feedback architecture: the equilibrium reproduces itself because the data the equilibrium generates appears to validate the criteria that produce it.

The AVCA 2026 Gender Diversity in African Private Capital report finds female-led companies grew revenue 32 percent in 2023–24, against 14 percent for male-led peers - outperforming on the metric investors claim to care about most while receiving a fraction of the capital. That this evidence has not materially changed investment behaviour is itself evidence that the evaluation framework is not primarily responsive to performance data. It is embedded in social and institutional structures that are resistant to purely evidential challenge.

Mechanism 5: The offshore incorporation gender filter.

The substantive treatment of the offshore incorporation dynamic and how it operates as a structural barrier to African ecosystem development sits in Political & Regulatory Barriers, Feedback Loops Loop 5, and The Political Economy of the Ecosystem. The implication for gender-scaling analysis is that the offshore-incorporation requirement that most international VCs impose as a condition of investment functions as an additional gender filter.

The social networks through which offshore incorporation advice, legal services, and structuring expertise flow are disproportionately male. The institutional investor relationships that make offshore structuring meaningful - access to Delaware-registered angel syndicates, Cayman Islands fund structures, and Silicon Valley investor networks - are embedded in the same social networks that generate the network access loop. The offshore incorporation requirement - a product of capital architecture mismatch rather than deliberate gender filter - functions as an additional screening mechanism that further reduces the proportion of female-founded ventures accessing international capital.

The interaction of the five mechanisms

The five mechanisms are not parallel - they are sequential and interacting. The network access loop determines which founders are seen. The evaluation bias feedback loop determines which of those founders are funded and at what amounts. The sector-stage trap determines the funding trajectory of those who are funded. The triple dissonance amplifier compounds the disadvantage at each step. The offshore incorporation filter adds a structural barrier at the point of international capital access. Each mechanism, individually, might be navigated by a sufficiently resourced and networked founder. The system, operating simultaneously through all five mechanisms, maintains the gap regardless.

What structural intervention requires

Addressing the network access loop requires changing how deal flow is generated, not just how it is evaluated - deliberate investment in alternative deal flow channels, female-founded referral networks, and LP requirements for GPs to demonstrate diverse deal flow sourcing rather than simply diverse portfolios. The AVCA 2026 report provides the structural evidence: firms with majority-female investment committees invest in significantly more women-led companies than their peers. Investment committee composition is the mechanism. It is the appropriate target for intervention.

The contemporary global standard for gender-lens capital allocation is the 2X Criteria - a framework developed by G7 DFIs at the 2018 Charlevoix Summit, updated to v2.0 in 2021 and substantially expanded in 2024 (adding Governance & Accountability and Supply Chain criteria) that establishes specific operational thresholds for gender-lens capital deployment: percentage female ownership, percentage female leadership representation, percentage female workforce, and percentage of products/services that disproportionately benefit women. The 2X framework is structurally consequential because it moves gender-lens investing from values-based commitment to operational thresholds that DFIs and other investors can apply across portfolios. The AVCA data suggests that investment-committee composition and fund-level gender practices are associated with stronger allocation to women-led companies, but the evidence should not be overstated as proof that 2X alone is changing DFI allocation. The question for African gender-lens capital deployment is whether commercial GPs adopt 2X-equivalent operational standards or continue to operate on values-based commitment without enforcement architecture.

Addressing the sector-stage trap requires changes to the investment thesis itself. Revenue-based financing, patient equity, and blended finance structures calibrated to the growth timelines of impact-adjacent sectors are structural alternatives to the standard VC model that are more compatible with the sectors where female founders are concentrated. Janngo Capital - founded by Fatoumata Bâ in 2018 with a gender-equal investment thesis (target 50 percent of capital in women-founded, co-founded, or female-benefiting ventures), with a realised portfolio that is 56 percent women-led across both funds - demonstrates this model in operation. Aruwa Capital and Alitheia IDF are building comparable portfolios. These are not charity vehicles. They are investment funds making market-efficiency bets on the performance paradox.

The 2025 research What Enables Her Business to Grow - developed through a collaboration between the Argidius Foundation, the Dutch Good Growth Fund, the Women Entrepreneurs Finance Initiative, and ConsumerCentriX - provides the most rigorous available segmentation framework for women-owned and led SMEs across Pakistan, Uganda, and Colombia. Its core finding directly challenges the binary framing of most gender-lens investment: rather than treating WSMEs as a single category, it identifies three growth segments (high, moderate, and low) and six distinct entrepreneur profiles within them, each with materially different financial and non-financial needs. The implication for capital allocation is precise: a gender-lens fund that deploys a single instrument across all six profiles is not doing gender-lens investing. It is doing gender-labelled investing. Effective intervention requires segment-specific product design - which the framework provides and which most African gender-focused capital vehicles have not yet adopted.

Addressing the evaluation bias feedback loop requires adoption of structured, evidence-based evaluation processes - data-driven due diligence tools that assess venture performance metrics rather than founder presentation styles, and standardised reporting that makes the performance paradox visible at the portfolio level.

Addressing the offshore incorporation gender filter requires locally-domiciled fund structures that do not require offshore incorporation as a condition of access - connecting directly to the capital architecture mismatch and the regulatory hostility trap identified in earlier sections.

The performance case, restated

The current system is systematically allocating capital away from higher-performing ventures. The failure is one of market efficiency, not values. A market that consistently underfunds its highest-performing segment while consistently overfunding its lower-performing segment is not functioning efficiently. The structural interventions described above are not about achieving equity at the cost of returns. They are about achieving returns by correcting the structural dysfunctions that prevent capital from flowing to its highest-performing uses.

Equity arguments have been made for a decade without reversing the trend. Performance arguments, made with rigorous evidence and directed at the structural mechanisms that generate the gap, create commercial incentives for change that equity arguments alone cannot generate. The TechCabal Insights Baobab Model analysis found that funding to startups with at least one female founder grew 81 percent in 2025, from $152 million to $275 million. This is a positive signal, but it should be read alongside Africa: The Big Deal’s CEO-level data, which still shows extremely low funding shares for women-led ventures. The structural gaps remain. The pace is what the ecosystem now has the capacity to change.