Capital Systems

Access to a range of financing instruments is critical for scale. African-specific evidence confirms that ventures not facing credit constraints grow faster than those that do - which justifies the sustained effort to increase capital availability. That justification is necessary but not sufficient. The structure of African capital - who holds it, who deploys it, on what terms, to whom, and through what institutional architecture - matters as much as the volume.

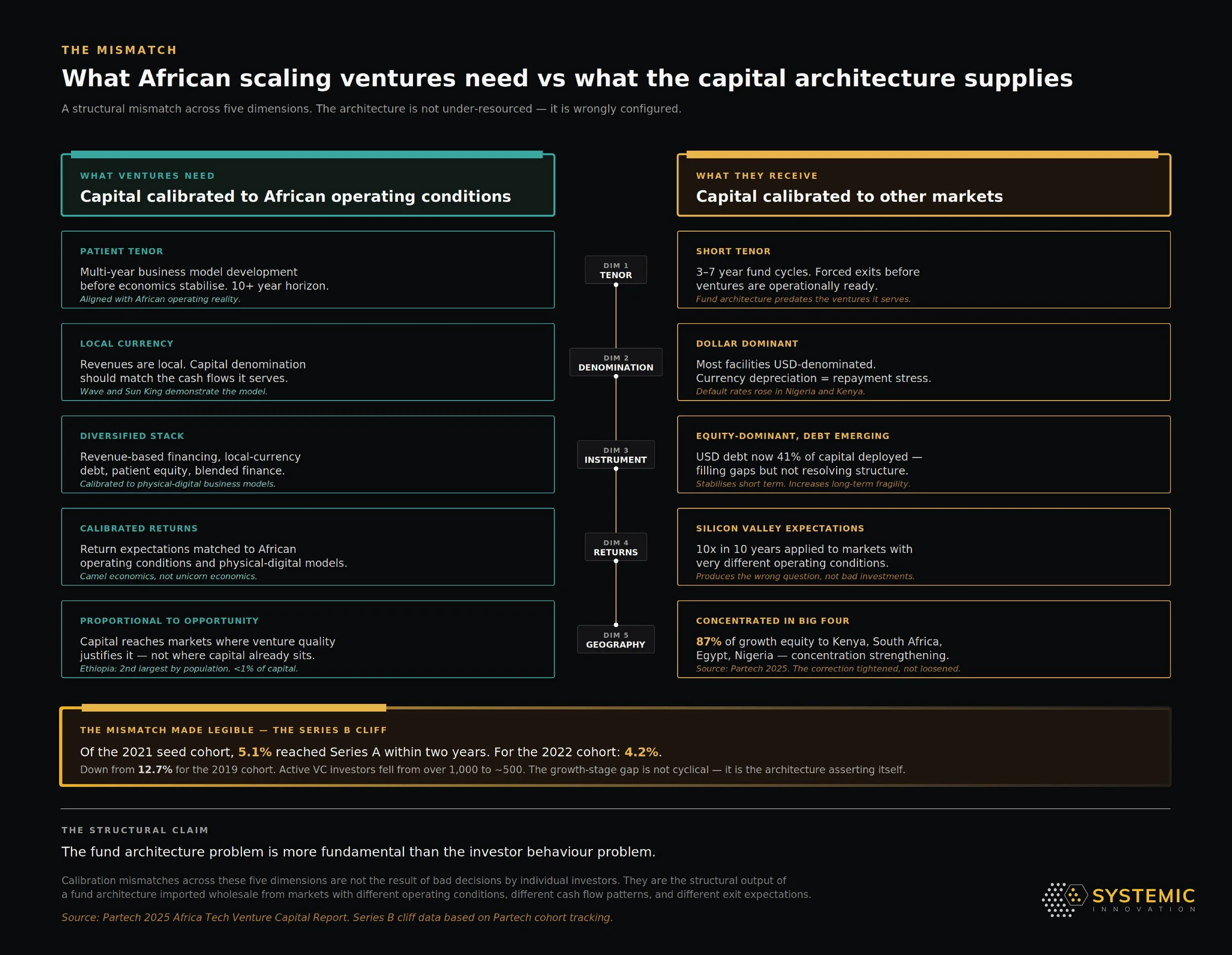

The substantive treatment of how this structural mismatch operates at the founder-decision layer - anchored in The Financing Journey Through the Scaling Phases - establishes the Series B cliff as the most consequential structural failure during the correction period. The graphic below sets out the mismatch at the chapter level: what African scaling ventures actually need against what the dominant capital architecture supplies. The correction period has provided something more useful than theory: empirical evidence about which parts of the capital architecture failed, which held, and why.

Calibration mismatches across these five dimensions are not the result of bad decisions by individual investors. They are the structural output of a fund architecture imported wholesale from markets with different operating conditions, different cash flow patterns, and different exit expectations. The fund architecture problem is more fundamental than the investor behaviour problem.

This is the analytical category emerging in DFI practice as market creation - most explicitly in FMO's 2030 Pioneer, Develop, Scale strategy, which distinguishes ecosystem building (regulatory environments, business support services, intermediary capacity) from business development (firm-level investment bottlenecks beyond financial management, ESG and collateral). The six-dimension architecture set out extends that frame from DFI bankability to firm-level scaling dynamics, intermediary capacity, and the architecture of patient capital.

This section examines the structural architecture across six dimensions: the investor landscape that determines what capital is actually available; the institutional actors whose mandates shape allocation; the investor propositions through which capital is deployed; the political economy of capital that explains why the mismatch persists despite widespread recognition; the founder's capital map that founders need to navigate the architecture in practice; and the investor-founder relationship through which the architecture operates at the venture-deal level. Each section examines a different layer of the capital architecture problem. Together they describe the system founders are operating in and the changes that would make it function differently.